| The changes to gambling regulation in the UK, coming into effect from 1 October 2014, have already started having an impact. Sites have been shutting their doors to UK customers pretty consistantly recently; Pinnacle, SBO and Sportsbook.com.au to name but a few. I understand that the additional taxation is also playing a part, but what are the actual regulatory changes that have bookmakers leaving this green and pleasant land? |

You probably haven't been interested enough in the process of regulation change, or the associated changes in the gambling act, to have looked in depth at the consultation documents. Honestly, nor had I. Until it started hitting my wallet and ability to make money from Matched Betting. First things first, matched betting and advantage play is still alive and well. There are still plenty of sites offering plenty of bonuses that can be played off against each other to profit from. But something has changed.

I took a look at the Gambling Commission website to see what I could find out on about the reg changes, when they'd be coming into effect, and what impact they might have on me, a customer (not a punter, that makes me sound like a mug!).

There were a number of consultations as part of the process to make the changes that will be coming into force. They gave operators the right to reply and state why they would recommend another course of action, or why the Gambling Commission had it wrong.

If you want to read all the consultations and the results then they are available in three parts covering the following the subjects: part 1 relating to complaints and disputes and information requirements, part 2 protection of customer funds and part 3 notification of suspicious activity.

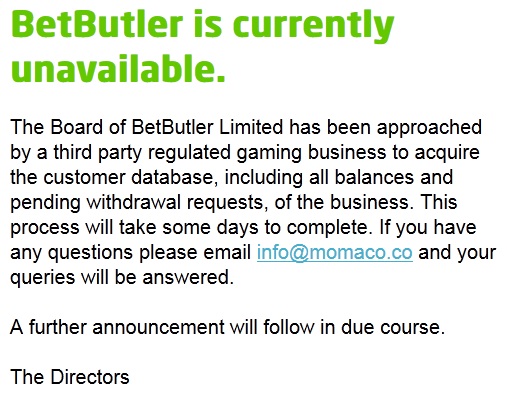

It's fair to say that overall these documents are fairly dry. The major change is around the need for all operators who are taking UK customers to apply for a licence from the Gambling Commission. There are, however, a few interesting points and ommissions in the second consultation document concerning protection of customer funds, particularly relevant given the issues the Gambling Commission have had this year with Canbet, Bodugi and BetButler.

I took a look at the Gambling Commission website to see what I could find out on about the reg changes, when they'd be coming into effect, and what impact they might have on me, a customer (not a punter, that makes me sound like a mug!).

There were a number of consultations as part of the process to make the changes that will be coming into force. They gave operators the right to reply and state why they would recommend another course of action, or why the Gambling Commission had it wrong.

If you want to read all the consultations and the results then they are available in three parts covering the following the subjects: part 1 relating to complaints and disputes and information requirements, part 2 protection of customer funds and part 3 notification of suspicious activity.

It's fair to say that overall these documents are fairly dry. The major change is around the need for all operators who are taking UK customers to apply for a licence from the Gambling Commission. There are, however, a few interesting points and ommissions in the second consultation document concerning protection of customer funds, particularly relevant given the issues the Gambling Commission have had this year with Canbet, Bodugi and BetButler.

Customer reaction to the situations, has demonstrated that there is a significant gap between the level of protection that customers and commentators assume they might receive (and which they assume regulators would have required) and the actual level of protection afforded.

This is the first time I've seen the Gambling Commission admit that a fundamental part of what the customer expects them to do is regulate the bookmakers and casinos in such a way as to offer customers some protection. Nice of them to catch up with the idea that regardless of what they do, they need to make it clear to all customers (not just the people that have read the reports on BetButler here and on The Gambling Times) what protection they offer.

Gamblers may have more appetite for risk.

Customers may not wish to bear the increased costs of protection and would rather assess companies individually.

However, such assessment is only possible if consumers are given sufficient, meaningful information.

Gamblers may have more appetite for risk, but that is in so much as the bets they place, not that the company might at any moment fold. Actually, that's probably not entirely fair, a professional gambler will weigh up the risk of using a bookmaker against the potential reward. The average man on the street won't be doing that. If a bookmaker is regulated by the Gambling Commission it implies that they are reputable and being watched with a beedy eye. Something that clearly hasn't been the case recently.

Worth also picking out from that statement is that customers require information to be able to make informed choices. I'm a big fan of The Rise and Fall of Canbet an article which tracked the withdrawal issues against the bonuses being offered in the run up to the company folding. Sharing the information on withdrawals and complaints allowed the majority of TGT customers to get out of Canbet without getting burnt. Anyone who was still in was aware of the risks. Again, the man on the street isn't aware.

Finally on this point, if the Gambling Commission is so keen on the sharing of information, then why do freedom of information act (FOIA) requests get declined? Information on how they have dealt with a failing bookmaker, what time lines are involved and how they respond to complaints would be incredibly useful information for both professional and mug punters.

Worth also picking out from that statement is that customers require information to be able to make informed choices. I'm a big fan of The Rise and Fall of Canbet an article which tracked the withdrawal issues against the bonuses being offered in the run up to the company folding. Sharing the information on withdrawals and complaints allowed the majority of TGT customers to get out of Canbet without getting burnt. Anyone who was still in was aware of the risks. Again, the man on the street isn't aware.

Finally on this point, if the Gambling Commission is so keen on the sharing of information, then why do freedom of information act (FOIA) requests get declined? Information on how they have dealt with a failing bookmaker, what time lines are involved and how they respond to complaints would be incredibly useful information for both professional and mug punters.

What is important is that the regulator takes all appropriate actions to mitigate the risks to consumer funds and/or to ensure that the consumer makes informed choices about the risks they are comfortable with.

Sounds like the bare minimum they should be doing. So what are the practical changes that will be made to protect customers?

Remote gambling operators must segregate customer funds into a separatebank account.

Visible and meaningful disclosure to customers to ensure that customers are not given false assurances about the level of risk which remains in the event of insolvency.

Let's be clear here, separation of client funds is not a guarantee that if they go under your funds are protected. All it means is that a bookmaker or casino would need to make a consious decision to dip into client funds instead of using their day to day operations account. Information on separation of client funds is already found in the T&Cs of all UK regulated operators, although you have to trawl through a lot of information to get to it.

The change is that from 1 October all customer funds will need to be held in segregated accounts, and that on first deposit (or after any change in the T&Cs related to segregation) there will be a message stating what level of protection client funds have in the event of insolvency. This could of course range from no protection, to a full trust situation where all funds would be protected (doubt many bookies will go for that given the additional cost of administrating such a system).

The change is that from 1 October all customer funds will need to be held in segregated accounts, and that on first deposit (or after any change in the T&Cs related to segregation) there will be a message stating what level of protection client funds have in the event of insolvency. This could of course range from no protection, to a full trust situation where all funds would be protected (doubt many bookies will go for that given the additional cost of administrating such a system).

Introduce a formal mechanism for reporting on the level of customer funds and where possible introduce an element of external verification of those reports where appropriate.

This is essentially the way the Gambling Commission will regulate to protect customers (though it doesn't come into effect until January 2015 at the earliest). The reporting required from the operators to the Gambling Commission will cover the disclosure of client funds held and notice of any key events that might impact on the client account.

Overall it seems the Gambling Commission are moving in the right direction with their regulation of the industry. It's still what you'd describe as light touch, but should limit the instances of the Canbets and BetButlers being left alone and able to run off with customer funds.

One final nugget from the consultations. The Gambling Commission propose.......

Overall it seems the Gambling Commission are moving in the right direction with their regulation of the industry. It's still what you'd describe as light touch, but should limit the instances of the Canbets and BetButlers being left alone and able to run off with customer funds.

One final nugget from the consultations. The Gambling Commission propose.......

.......a new ordinary code provision to make explicit our expectation that operators work with us in an open and cooperative manner

That's right, they're going to put down in writing that operators must deal with them in an open and cooperative manner. Makes you wonder what BetButler (although we may already know!) were doing if this needs to be written down. The response from the consultation on this was mixed. Some operators said it didn't need to be written down, it was already implied and they were doing it, but........

Some respondents felt that the fact such a requirement was not already in was a serious flaw

So there you have it, that's the summary of the changes. Nothing too shocking, which leads me to believe that actually it's the point of consumption tax coming at the end of the year that's really driving bookmakers and casinos away from the UK market.

You're also still not going to get that much assistance from the Gambling Commission so if you want to protect yourself, share information on The Gambling TImes about your withdrawal experience, what bonuses are being offered and what the customer serivce is like. All three are potential flags for there being an issue with the operator, but we won't know unless we share.

You're also still not going to get that much assistance from the Gambling Commission so if you want to protect yourself, share information on The Gambling TImes about your withdrawal experience, what bonuses are being offered and what the customer serivce is like. All three are potential flags for there being an issue with the operator, but we won't know unless we share.

RSS Feed

RSS Feed